Comment on David Glasner on ‘Does Economic Theory Entail or Support Free-Market Ideology?’

Blog-Reference and

Blog-Reference on Jan 18 adapted to context

Economics of the last 200+ years is the most embarrassing failure in the history of modern science.

The basic question of economics is whether “the existing economic system is, in any significant sense, self-adjusting.” (Keynes) Walrasian economics failed to prove this. The lethal methodological blunder of standard economics has been to put equilibrium (and other nonentities) into the premises. This blunder is known since antiquity as

petitio principii.#1

Keynes realized that the classical microfoundations approach had led into a cul-de-sac and therefore switched to macrofoundations. This was ― in principle ― the right first step towards a

Paradigm Shift, except for the fact that Keynes messed up his macrofoundations. This is why Keynesianism, too, is a failure.#2

Because the four main approaches ― Walrasianism, Keynesianism, Marxianism, Austrianism ― are mutually contradictory, axiomatically false, and materially/formally inconsistent, economic policy guidance never had sound scientific foundations from Adam Smith/Karl Marx onward. This applies, of course, to the so-called free-market ideology.

There is political economics and theoretical economics. The main differences are: (i) The goal of political economics is to successfully push an agenda, the goal of theoretical economics is to successfully explain how the actual economy works. (ii) In political economics anything goes; in theoretical economics, the scientific standards of material and formal consistency are observed.

Economics claims to be a science but is NOT. Theoretical economics (= science) had been hijacked from the very beginning by political economists (= agenda pushers). Political economics is scientifically worthless. It is pretty obvious that Keynes, Hayek,#3 Friedman,#4 etcetera were not scientists but clowns in the political Circus Maximus.

True economic theory tells us how the economic system works. The economist needs the true theory, i.e. the humanly best mental representation of reality: “In order to tell the politicians and practitioners something about causes and best means, the economist needs the true theory or else he has not much more to offer than educated common sense or his personal opinion.” (Stigum)

Keynes, Hayek, Friedman, and their heirs/parrots up to DSGE and MMT never rose above the proto-scientific level of common-sense rhetoric, opinion, and political agenda pushing. The claim as expressed in the title “Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel” is a joint Walrasian/Keynesian/Marxian/Austrian deception of the public.

Egmont Kakarot-Handtke

#1

Petitio principii — economists’ biggest methodological mistake

#2

What Keynes really meant but could not really prove

#3

Austrian idiocy ― the case of Hayek

#4

Milton Friedman, fake scientist

***

***

Skidelsky concludes: “Macroeconomics still needs to come up with a big new idea.”

■ Public Deficit = Private Profit ― is Keynesianism/MMT a social hoax?

■ Paradigm Shift is the big new idea

***

REPLY to Ralph Musgrave on Jan 21

You say “Even if every dollar of stimulus did end up in the pockets of the rich, that would not stop stimulus working. To illustrate, assume 10% of all government spending ends up as profit which is hoarded by the rich. That means 90% initially goes to the “non-rich”. In the next ‘round’ so to speak, 10% is again hoarded by the rich.”

This is a nice try playing down the fact that Public Deficit = Private Profit and that, by consequence, MMT is essentially a social bluff package for the agenda of the one-percenters.

Your error/mistake/blunder consists of applying the old Keynesian multiplier which, unfortunately, is false for 80+ years.#1, #2, #3

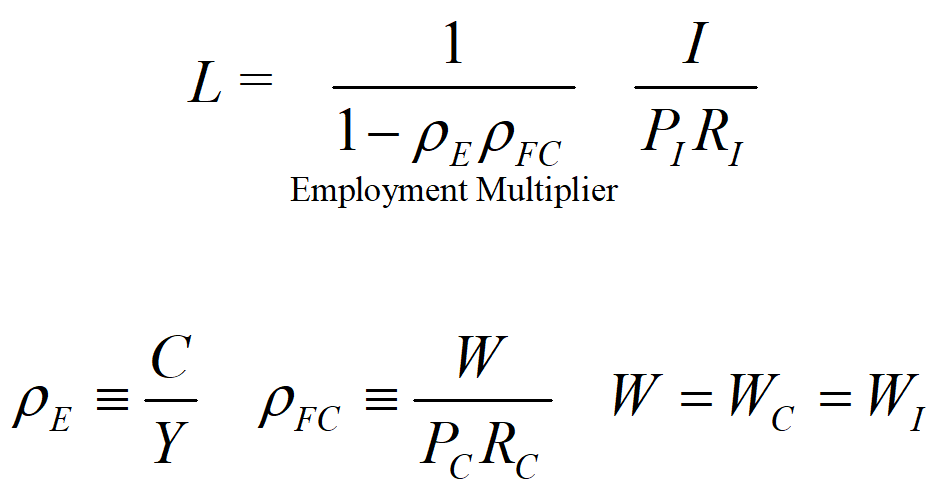

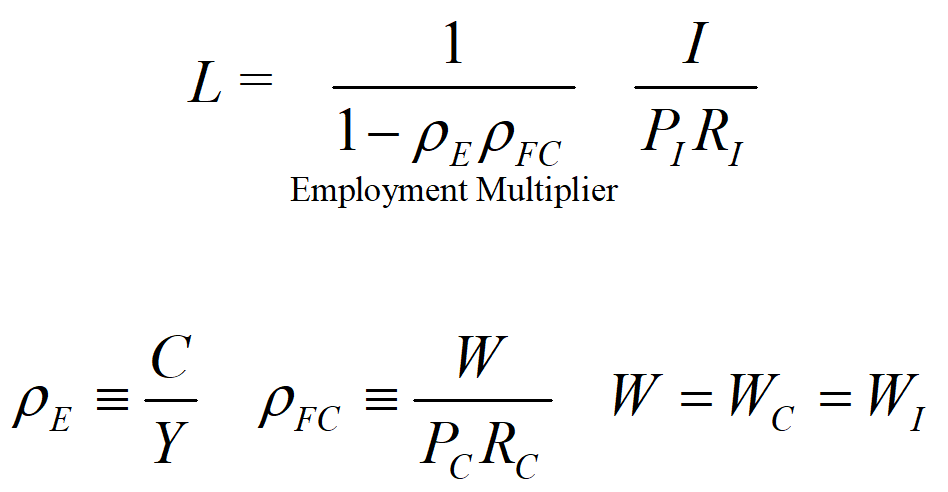

To cut the meticulous formal derivation short, the most elementary version of the

axiomatically correct

Employment Law for the economy as a whole is given on Wikimedia

AXEC62:

From this equation follows:

(i) An increase in the expenditure ratio ρE leads to higher employment L (the Greek letter ρ stands for ratio). An expenditure ratio ρE greater than 1 indicates credit expansion, a ratio ρE less than 1 indicates credit contraction of the household sector.

(ii) Increasing investment expenditures I exert a positive influence on employment, a slowdown in growth does the opposite.

(iii) An increase in the factor cost ratio ρF≡W/PR leads to higher employment.

The complete Employment Law is a bit longer and contains in addition profit distribution, public deficit spending, and import/export.

The correct employment multiplier consists of TWO elements: the expenditure ratio and the factor cost ratio. Now, the following may happen simultaneously: the expenditure ratio goes up and the factor cost ratio goes down such that the combined multiplier effect is zero. That means, deficit spending has NO effect on employment but only on profit. All that is necessary for annihilating the employment effect of deficit spending is a one-off price hike.

So, deficit spending ALWAYS benefits the one-percenters because Public Deficit = Private Profit is absolutely certain while the employment effect is very uncertain and may well be zero.

***

REPLY to Tom Hickey on Jan 21

You say “I can see how Egmont might be right about government deficits ended up as money in the elites pockets. MMT says essentially the same thing. Government deficits accommodate non-government saving, most of which is done by those that are well-off if not rich.”

The smarter part of humanity, in turn, can see now that you, Kaivey, Musgrave, Kelton, Mosler, Mitchell, Tcherneva, Wray, Fullwiler, Forstater, Kaboub, Pettifor, Keen, Tymoigne, Willingham, Grumbine, and all the blogging and tweeting MMT rest have NO idea how the economy works.

The

axiomatically correct balances equation reads

Qm≡Yd+I−Sm+(G−T)+(X−M); Legend: Q

m total monetary profit, Y

d distributed profit, I investment expenditures, S

m monetary saving, G government expenditures, T taxes, X exports, M imports. This translates into

Public Deficit = Private Profit given the balances of the other sectors.#1

The government deficit does NOT “accommodate” household sector saving Sm because the household sector as a whole may also run a deficit = dissaving = Sm negative. In this case, it holds macroeconomic profit = public sector deficit PLUS household sector deficit. And exactly this was the case in the USA in the last decades.

The MMT headline government deficit = private sector surplus is proto-scientific garbage or worse.#2

***

REPLY to Tom Hickey on Jan 22

You say “According to MMT, the way to moderate capitalism is through increasing the welfare state, increasing labor bargaining power, and adding a JG. This would preemptively distribute wages so that rising incomes could sustainable consumption desire at full employment.”

In the political realm, everybody can climb on a soapbox and tell the audience how the world can be made a better place and how the economy can be fixed ― except an economist.

The mission of the economist ― understood as a scientist ― is to figure out how the economy works and NOT to push a political agenda. The monstrous failure of both orthodox and heterodox economists is that they have NOT developed anything resembling the true theory in the last 200 years but crawl in endless loops in the proto-scientific swamp. MMT is just a case in point.

Because they do not have the true (= materially and formally consistent) theory economists’ contribution to policy is worthless or even counterproductive. It is just like the storytellers of old who never contributed anything to aviation but only entertained their audience with tales about flying carpets.

In the political realm, MMT is the deficit-does-not-matter storyteller, but in the scientific realm MMT does not even get the elementary mathematics of macroeconomic accounting right.#1

MMT’s claim to rectify capitalism is laughable. MMT is a flying carpet story just like Walrasianism, Keynesianism, Marxianism, and Austrianism.#2