Comment on James Galbraith on ‘Reconsideration of Fiscal Policy: A Comment’*

COVID-19 is a godsend for the Oligarchy. The 3-sector macroeconomic Profit Law Q≡(G−T)+(I−S)+Yd implies Public Deficit (G−T) = Private Profit Q. The current acceleration of deficit-spending/money-creation will result in the biggest profit explosion ever.

Government deficit-spending, of course, increases public debt, and it roughly holds: Financial assets of the Oligarchy ≈ Public debt of WeThePeople. As a result, the inequality of income/wealth increases in the process.#1

While not much can be said against short-term deficit spending in an emergency situation, some people are concerned about the longer-term effects of a continuously increasing public debt. MMTers, the proponents of permanent deficit-spending/money-creation, claim that there is nothing to worry about and that the debt hysteria over several centuries was just that: much ado about an economic non-event.

Because MMT is a refuted approach and MMTers are agenda pushers for the Oligarchy, their arguments have to be taken as tranquilizers for the general public. The question of whether there is an upper limit for public debt is still open. Economists have come up with the answer that there is nothing to worry about as long as the economy grows faster than the debt, i.e., r < g, which is as trivially true mathematically as it is idiotic economically.

Neither mainstream economics nor MMT has a valid scientific foundation. So the macroeconomic analysis of deficits and debt must first be based on correct premises.

As the new analytical starting point, the elementary production-consumption economy is defined with this set of macroeconomic axioms‡: (A0) The objectively given and most elementary configuration of the economy consists of the household and the business sector, which in turn consists initially of one giant fully integrated firm. (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

Under the conditions of market-clearing X=O and budget-balancing C=Yw in each period, the price is given by P=W/R, i.e., the market-clearing price is determined by the wage rate, which takes the role of the nominal numéraire, and the productivity. This is the most elementary form of the macroeconomic Law of Supply and Demand. For the graphical representation, see Figure 1.#2

Monetary profit for the economy as a whole is defined as Q≡C−Yw, and monetary saving is defined as S≡Yw−C. It always holds Q≡−S, in other words, the business sector’s profit Q equals the household sector’s dissaving −S. Vice versa, the business sector’s loss −Q equals the household sector’s saving. This is the most elementary form of the macroeconomic Profit Law.

With the government included, the Profit Law reads Q≡(G−T)−S+Yd. And under the condition of S=0, Yd=0, one gets Public Deficit = Private Profit. So, the public sector's deficit reappears one-to-one as monetary profit of the business sector. If the public sector issues bonds to cover the deficit, the business sector has the exact amount at hand to buy them, no matter how large the public deficit is.

To simplify things, it is assumed that the profit of the business sector is fully distributed to the owners, i.e., the Oligarchy. Distributed profit is not spent but used to buy government bonds. The receivers of distributed profit income Yd, and the receivers of wage income Yw make up the household sector.

In the first period, the state sector spends G, and taxes T are zero, so deficit spending equals G, and for the profit of the business sector holds Q equals G. This profit is distributed, so Yd equals Q. Total income of the household sector is Yw+Yd, and C=Yw and S=Yd.

In the next period, public expenditures increase because of the interest on public debt. This amount is taxed from the wage income receivers and paid out to the bondholders, i.e., to the Oligarchy. The disposable income of WeThePeople is reduced Yw−T, and that of the Oligarchy is increased Yd+T. The budget deficit remains the same (G+T)−T. The Oligarchy spends T on consumption, so total demand does not change.

In principle, this simplified process of deficit-spending/money-creation can continue period after period. What happens is that public debt increases continuously, and with it the interest = tax payments of WeThePeople.

The debt is not paid back, so it has to be rolled over at maturity. To avoid this, the government can issue perpetual bonds. The problem remains that interest = tax T sooner or later becomes equal to wage income Yw, and the disposable income of the wage income receivers approaches zero. So, there is an absolute upper limit for the growth of debt. This limit vanishes only if the interest rate on perpetual bonds is zero. However, a debt that is never repaid and yields no interest is not a debt but a gift. For a gift economy, the MMT assertion that the amount of public debt does not matter is trivially true.

As long as the interest rate on perpetual bonds is greater than zero, there is an upper limit for the growth of public debt. This limit may be so far in the future that it is not of practical importance for the present generation, but just because it is beyond the time horizon, it remains.

Vice versa, if the interest rate rises in the process, the debt limit is reached faster. A higher interest rate on an increased debt reduces the debt limit exponentially. The debt trap is snapping shut.

As a matter of fact, with growing public debt and a positive interest rate on perpetual bonds, the disposable income of WeThePeople falls continuously from the present onward, and their living standard continuously deteriorates. The never-mentioned negative distributional effects are the ultimate reason why the MMT policy of permanent deficit-spending/money-creation is a political fraud.#3, #4

Egmont Kakarot-Handtke

‡ Reminder: The Axioms and Laws are protected by Trademark®. For details, see

Terms of Use.

***

***

Twitter

Mar 11 Interest payments in comparison

Twitter

Mar 11 Interest rates, interest costs

Twitter

Mar 18 Interest payments as a share of household income

Twitter

Mar 20 Share of public debt owned by the one-percenters aka size of the cash cow

Twitter

May 20 Another attempt to optically reduce the interest burden of WeThePeople by relating it to a big number

Twitter

May 30 Next attempt to fudge the interest burden of WeThePeople

Twitter

Sep 13 Future debt service payments

Twitter

Oct 14 Average interest rate on public debt

Twitter

Nov 11 Debt-to-GDP ratio and interest payments as a percentage of GDP

Twitter Jun 28, 2022 As expected, after interest rates at the zero lower bound and a massive increase in public debt, bondholders now get a rise

Twitter/X Apr 17, 2024

Twitter/X

Jul 8, 2024, It's deficit spending, Elon, not government spending as such

Twitter/X

Jul 11, 2024 "Can anyone explain to me how this could possibly end well?"

Twitter/X

Aug 11, 2024 The #FreeMarketEconomy runs on private and public deficit-spending/money-creation ― for a while

Twitter/X

Oct 19, 2024 Elon Musk sounds the alarm ― too late

Twitter/X

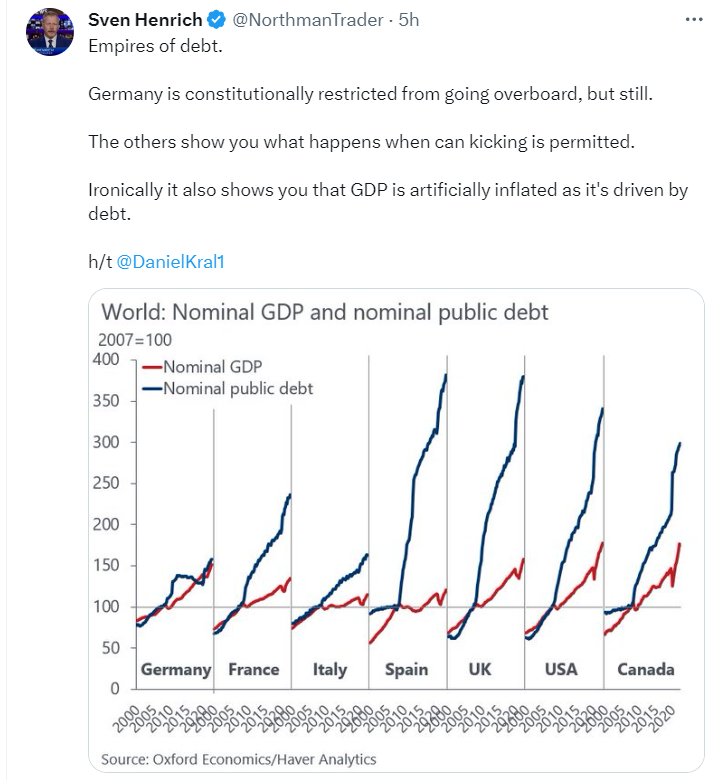

Feb 26, 2025, The absolute debt limit is fast approaching

Twitter/X

May 8, 2025 Here we are: maturity → ∞, interest → 0

Twitter/X

Nov 5, 2025 Pretty-face economics about interest