#Economics#AllYouNeedToKnow

— AXEC (@EgmontHandtke) March 3, 2025

There is a grave error in Richard Wagner's attached statement on retirement saving.

It is NOT the case that saving governs investment or that investment governs saving or that both are equal by definition. Both are independent and they together… pic.twitter.com/euV9jsq8Nn

Showing posts with label Investment. Show all posts

Showing posts with label Investment. Show all posts

March 3, 2025

Occasional Xs: Since Keynes' I=S, economists get saving and profit wrong (II)

October 1, 2024

Occasional Xs: What economists really do (CCCLX)

#Economics#FailedFakeScience

— E.K-H (@AXECorg) October 1, 2024

“Ohne Schulden hat noch niemand eine Eisenbahn gebaut” (Philippa Sigl-Glöckner, Ökonomin)

True, but entirely beside the point. Ms. Sigl-Glöckner plays a silly mind game by confusing the debt-financing of infrastructure and the debt-financing of…

Also at Christian Breuer.

April 15, 2024

Occasional Xs: What economists really do (CCXV)

#LearnRealEcon

— E.K-H (@AXECorg) April 15, 2024

Since 2018, the Trump and Biden administrations have lifted the #DebtCeiling several times. Did this help to significantly improve public infrastructure, alleviate poverty, or improve the future of American children?

No.

But because of the 3-sector #ProfitLaw… pic.twitter.com/tdwvENngDK

October 16, 2022

Occasional Tweets: What is "late-stage capitalism" exactly?

#Economics

— E.K-H (@AXECorg) October 16, 2022

The 3-sector #ProfitLaw Q≡(G−T)+(I−S)+Yd implies #PublicDeficitIsPrivateProfit. Thus, #DeficitSpendingMoneyCreation is a #FreeLunch for the #Oligarchy. Growing #PublicDebt is the life elixir of #LateStageCapitalism. In the earlier days, it was the (I−S) component. pic.twitter.com/CnnSdjFTYg

March 1, 2019

Dear idiots, time to get saving and investment straight (II)

Comment on Lars Syll on ‘Krugman vs Kelton on the fiscal-monetary tradeoff’

Blog-Reference and Blog-Reference

Murray Rothbard argued: “In short, what can help a depression is not more consumption, but, on the contrary, less consumption and more savings (and, concomitantly, more investment).”

Charlie Price argued: “… you can’t create investment by saving. In fact, attempts at saving will reduce investment.”

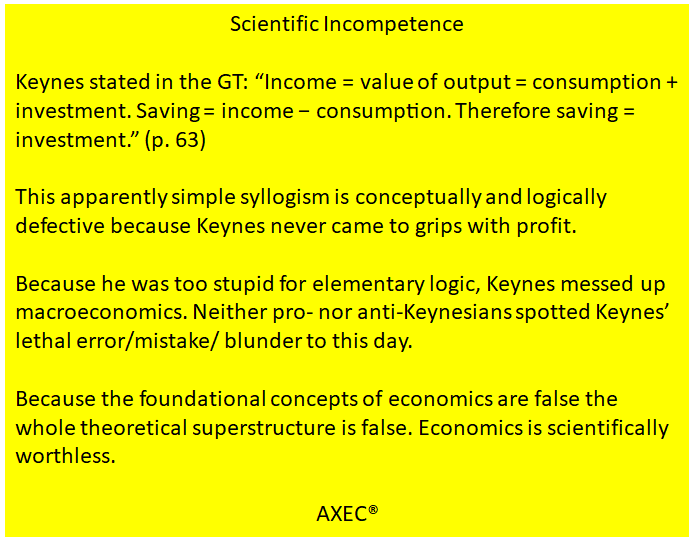

Keynes argued: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (GT, p. 63).

Here is the short proof that economists are to this day too stupid for the elementary mathematics that underlies macroeconomics.

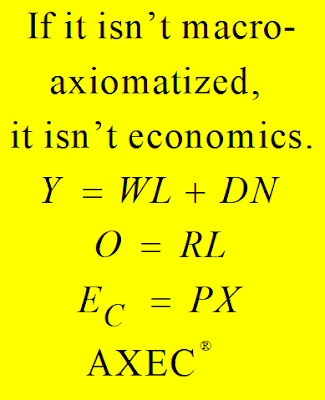

(i) The elementary production-consumption economy is given by three macroeconomic axioms: (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

(ii) The focus is here on the nominal/monetary balances. For the time being, real balances are excluded, i.e. X=O.

(iii) The monetary profit of the business sector is defined as Q≡C−Yw,

(iv) The monetary saving of the household sector is defined as S≡Yw−C.

(v) Ergo Q+S=0 or Q=−S.

The balances add up to zero. The counterpart of household sector saving S is business sector loss −Q. The counterpart of household sector dissaving (-S) is business sector profit Q. Both Q and S are measurable with the precision of two decimal places.

From (v) follows immediately that saving is NEVER equal to investment.#1, #2, #3, #4

For the elementary investment economy holds Q=I−S. From this follows that (1) saving and investment are causally INDEPENDENT and NEVER equal, (2) all I=S/IS-LM models are false since Keynes/Hicks, (3) Keynesianism, Post-Keynesianism, New Keynesianism and all variants are scientifically worthless, (4) the foundational MMT sectoral balances equation (I−S)+(G−T)+(X−M)=0 is provably false, (5) by consequence, the whole of MMT is false.

Lacking sound scientific foundations on both sides, the Krugman/Kelton debate is just one of those brain dead proto-scientific wrestling shows economists are known for since 200+ years.

Egmont Kakarot-Handtke

#1 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

#2 Settling the Theory of Saving

#3 Squaring the Investment Cycle

#4 For details of the big picture see cross-references Refutation of I=S

Related 'Krugman vs MMT ― like the blind talking about colors' and 'Dear idiots, time to get saving and investment straight (I)' and 'Macro for dummies (I)' and 'Macro for dummies (II)' and 'Wikipedia and the promotion of economists’ idiotism (II)' and 'Keynes and the logical brilliance of Bedlam' and 'Either stupid or duplicitous' and '#DrainTheScientificSwamp'.

Blog-Reference and Blog-Reference

Murray Rothbard argued: “In short, what can help a depression is not more consumption, but, on the contrary, less consumption and more savings (and, concomitantly, more investment).”

Charlie Price argued: “… you can’t create investment by saving. In fact, attempts at saving will reduce investment.”

Keynes argued: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (GT, p. 63).

Here is the short proof that economists are to this day too stupid for the elementary mathematics that underlies macroeconomics.

(i) The elementary production-consumption economy is given by three macroeconomic axioms: (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

(ii) The focus is here on the nominal/monetary balances. For the time being, real balances are excluded, i.e. X=O.

(iii) The monetary profit of the business sector is defined as Q≡C−Yw,

(iv) The monetary saving of the household sector is defined as S≡Yw−C.

(v) Ergo Q+S=0 or Q=−S.

The balances add up to zero. The counterpart of household sector saving S is business sector loss −Q. The counterpart of household sector dissaving (-S) is business sector profit Q. Both Q and S are measurable with the precision of two decimal places.

From (v) follows immediately that saving is NEVER equal to investment.#1, #2, #3, #4

For the elementary investment economy holds Q=I−S. From this follows that (1) saving and investment are causally INDEPENDENT and NEVER equal, (2) all I=S/IS-LM models are false since Keynes/Hicks, (3) Keynesianism, Post-Keynesianism, New Keynesianism and all variants are scientifically worthless, (4) the foundational MMT sectoral balances equation (I−S)+(G−T)+(X−M)=0 is provably false, (5) by consequence, the whole of MMT is false.

Lacking sound scientific foundations on both sides, the Krugman/Kelton debate is just one of those brain dead proto-scientific wrestling shows economists are known for since 200+ years.

Egmont Kakarot-Handtke

#1 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

#2 Settling the Theory of Saving

#3 Squaring the Investment Cycle

#4 For details of the big picture see cross-references Refutation of I=S

Related 'Krugman vs MMT ― like the blind talking about colors' and 'Dear idiots, time to get saving and investment straight (I)' and 'Macro for dummies (I)' and 'Macro for dummies (II)' and 'Wikipedia and the promotion of economists’ idiotism (II)' and 'Keynes and the logical brilliance of Bedlam' and 'Either stupid or duplicitous' and '#DrainTheScientificSwamp'.

***

#PointOfProof

Mar 1

Mar 1

January 26, 2019

Both Austrianism and MMT are proto-scientific garbage

Comment on Robert Murphy on ‘The Upside-Down World of MMT’*

Blog-Reference and Blog-Reference

For his refutation of MMT, Robert Murphy takes the MMT balances equation as the analytical starting point.

“That is the three balances have to sum to zero. The sectoral balances derived are:

• The private domestic balance (I−S)

• The Budget Deficit (G−T)

• The Current Account balance (X−M).

A simplification is to add (I−S)+(X−M) and call it the non-government sector. Then you get the basic result that the government balance equals exactly $-for-$ … the non-government balance (the sum of the private domestic and external balances). This is also a basic rule derived from the national accounts and has to apply at all times.”

“So … we derive this equation: G−T=S−I. That is, the amount of government spending minus total tax revenue, is necessarily equal to private saving minus private investment. The MMTers might succinctly express this relationship in words: Government Budget Deficit = Net Private Saving.”

After this first demonstration of his scientific incompetence, Robert Murphy goes on: “This is the fundamental problem with relying on macro-accounting tautologies; people often bring in causal arguments from economic theories without realizing they are doing so. Let’s look again at the equation causing so much confusion: G−T=S−I. As a free-market economist, I don’t need to run from this tautology. I can use it to underscore the familiar ‘crowding out’ critique of government deficit spending.”

No, the fact of the matter is that the so-called “macro-accounting tautologies” are provably false because economists are too stupid for the elementary mathematics that underlies macroeconomic accounting.#1

To make a long story short, the correct macroeconomic relations are given as follows:#2

(1) Q≡−S in the elementary production-consumption economy,

(2) Q≡I−S in the elementary investment economy,

(3) Q≡Yd+I−S in the investment economy with profit distribution,

(4) Q≡Yd+(I−S)+(G−T)+(X−M) in the general case with government in an open economy.

Legend: Q profit, S saving, I investment, Yd distributed profit, G government expenditure, T taxes, X/M foreign trade.

The simplification of (4) yields Q=(I−S)+(G−T) (i) and this compares to Robert Murphy’s (G−T)=(S−I) resp. 0=(I−S)+(G−T) (ii).

The upshot is that (ii) implies that macroeconomic profit Q is zero. And this is plain analytical idiocy because a zero-profit economy does NOT exist. All this proves that Robert Murphy does not understand how the market economy works. The word profit does not appear once in his post. Austrianism is the failed attempt of explaining the market economy without ever mentioning the foundational economic concept profit which is objectively given with the precision of two decimal places.

Robert Murphy’s “Government Budget Deficit = Net Private Saving” has to be corrected to “Public Deficit = Private Profit”. And this correct formula tells everyone that MMT is a political fraud.#3

Robert Murphy, of course, does not realize anything. Austrians, in general, are not very smart. Because of this, Austrianism has never been anything else than vacuous proto-scientific blather.

Egmont Kakarot-Handtke

* Mises Institute

#1 Wikipedia and the promotion of economists’ idiotism

#2 Rectification of MMT macro accounting

#3 Stephanie Kelton’s legendary Plain-Sight-Ink-Trick

***

REPLY to Bob Roddis on Jan 27

“Research is, in fact, a continuous discussion of the consistency of theories: formal consistency insofar as the discussion relates to the logical cohesion of what is asserted in joint theories; material consistency insofar as the agreement of observations with theories is concerned.” (Klant)

Austrians are a political sect. Hayek’s Road to Serfdom is a political pamphlet with zero scientific content. What comes in the cloak of economic theory is thinly veiled agenda-pushing.

The foundational tenet ― markets never fail if left alone ― has no empirical content. It is only good for blaming any crisis on some random interventionist. The very characteristic of Austrians is circular reasoning. Circular reasoning is irrefutable and Austrians advertise this as strength ignoring the well-known methodological fact that a theory that is non-refutable is not scientific.

The foundational tenet of Austrianism has been refuted. The market system is inherently unstable because the relationship of wage rate and employment constitutes a positive feedback loop. When the foundational premise is false all the rest is scientifically worthless.

Robert Murphy’s discussion of the MMT sectoral balances equation proves that he does not understand elementary algebra and never realizes that the equation represents a zero-profit economy.

Austrians are simply too stupid for science. From von Mises onward to Hayek to Robert Murphy to Bob Roddis they are active as useful idiots in the political Circus Maximus.

***

REPLY to Bob Roddis on Jan 27You ask rhetorically: “Investment causes savings. Right. What do have to invest if you haven’t saved it?”

The relation between saving and investment is not well understood for 200+ years. This is disqualifying for the whole profession of academic economists.

Above, Robert Murphy tries to “explain the importance of saving and investment in a barter economy” and concludes “This is an admittedly simple story, but it gets across the basic concepts of income, consumption, saving, investment, and economic growth.”

No, not at all. Real models have always been garbage. A barter economy is a NONENTITY. The subject matter of economics is, as Keynes put it, the “monetary theory of production”. Starting with the right foot, however, Keynes messed up macroeconomics and ended up with I=S.

I=S is provably false. Keynesianism is refuted.#1

The correct relationship is given in the most elementary case as Q≡I−S, Legend: Q business sector’s monetary profit, I business sector’s investment expenditures, S household sector’s monetary saving. All variables are measurable with the precision of two decimal places.

The equation tells one that the household sector’s saving and the business sector’s investment are independent and that their difference determines profit/loss of the business sector as a whole.

In a fiat money system, saving S ends up as deposits at the central bank (if private banks are taken out of the picture for a moment). Investment I is financed by the central bank through credit creation and ends up as long-term debt on the asset side of the central bank’s balance sheet. Profit Q ends up as deposits on the liability side. Needless to emphasize that the central bank’s balance is balanced. However, the term structure of both sides is not congruent. The liability side of the central bank, i.e. the household’s and business sector’s deposits, constitutes money.

The households can, in a second step, either keep their deposits or buy the business sector’s stocks/bonds on issuance. This destroys money and shortens the central bank’s balance sheet.

Both, the Austrian idea that saving is the precondition of investment and the Keynesian idea that investment creates saving via the income multiplier is nonsense. In a fiat money system, saving S and investment I are independent. There is no causality, no equality, no equilibrium. This is what Q=I−S tells those who can read a simple macroeconomic equation.

#1 Cross-references Refutation of I=S

***

REPLY to Bob Roddis on Jan 27

Robert Murphy writes: “To explain the importance of saving and investment in a barter economy, I walk through a simple numerical example where Crusoe can gather ten coconuts per day with his bare hands.”

I respond: “A barter economy is a NONENTITY.”

You respond: “Actually, David Graeber, of all people, helped to improve and clarify the basic story because there was never a barter economy.”

So, we agree that Robert Murphy’s story about saving and investment is as silly as can be.

The real economy is NOT the ‘real’ barter economy but the monetary economy.#1 The economy constitutes itself through the interaction of real and nominal variables.

This interaction is defined with this set of macroeconomic axioms: (A0) The economy consists of the household and the business sector which, in turn, consists initially of one giant fully integrated firm. (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

Under the conditions of market-clearing X=O and budget-balancing C=Yw, the price is given by P=W/R. This is the macroeconomic Law of Supply and Demand.

Profit for the economy as a whole is defined as Q≡C−Yw and saving as S≡Yw−C. It always holds Q≡−S, i.e. the business sector’s profit is equal to the household sector’s dissaving, and the business sector’s loss is equal to the household sector’s saving. Under the initial condition of budget balancing, profit is zero.

So, the counterpart of household sector’s saving is business sector’s loss AND NOT INVESTMENT! Get it Austrians, we are living in a monetary economy and saving is NOT some non-consumed coconuts but money in the bank.

Austrianism is dead since about 1900. Now, rest in peace Bob Roddis and the Mises Institute.

#1 The irreparable unreality of all ‘real’ models

Related 'Settling the Theory of Saving' and 'Squaring the Investment Cycle'.

***

Switch to ‘Jennifer Morgan and Sharan Burrow — Tackling The Twin Challenges Of Climate Change And Inequality’

***

REPLY to Bob Roddis on Jan 29There is political agenda pushing and there is science. Economics as science tries to figure out how the monetary economy works. Austrian economics is proto-scientific garbage and a smokescreen for agenda pushing which comes under the euphemistic heading of Libertarianism.

Clearly, Austrians violate the principle of separation of politics and science since von Mises.

Your discussion of defensive or aggressive violence has no economic content. Worse, it misses the point. Compared to open violence, continuous low-intensity aggression/violence is currently the greater problem.

The upshot is, that this type of almost imperceptible violence is built right into the price system. And this brings us back to the heart of economics.

Contrary to Hayek, the major function of the price mechanism is NOT information processing and signaling but imperceptible redistribution. What is advertised as optimal functioning of an anonymous and apparently non-violent market system is, in fact, an impenetrable mechanism of continuous low-intensity redistribution.#1

To paint the market system as a superior information processor instead of a merciless slow-motion executor is one of the greatest deceptions of Austrianism.

#1 Pareto-efficiency, Hayek’s marvel, and the invisible executor

October 30, 2018

What comes first: eco-self-destruction or oeco-self-destruction?

Comment on Sandwichman on ‘Business As Usual: Running on Empty’

Blog-Reference

Ecological self-destruction is the subject matter of physics, biology, climatology, etcetera. Economists have nothing to say about these scientific issues because they are simply too incompetent for science. Economics is, after 200+ years, still at the proto-scientific level.

To make matters short, the central economic question is: Is the monetary economy sustainable on its own terms, that is, even if it faces no physical limits? The answer is NO.

Let us agree that, roughly speaking, the monetary economy as we know it can only exist if macroeconomic profit is positive and that the economy will break down if macroeconomic profit turns to loss. So, the question is, can it happen? and in case yes, when will it happen?

Now, the axiomatically correct macroeconomic Profit Law says Q≡Qm+Qn (i) with Qm≡Yd+(X−M)+(G−T)+(I−Sm) (ii) which simplifies to Qm≡I−Sm (iii) if Qn, Yd, X, M, G, T is set to zero.#1 Eq. (iii) says that monetary profit Qm is positive as long as the business sector’s investment expenditures are greater than the household sector’s saving. Or, if the household sector’s budget is balanced in each period, i.e. Sm=0 ⇒ Qm=I (iv), and this means that monetary profit Qm is positive as long as investment expenditures are positive (depreciation is a sub-item of Qn). In other words, the economy must grow or it drops dead. This may happen before the economy reaches the physical limits of growth.

The basic message of the Profit Law is that the monetary economy gets in trouble as soon as economic growth, expressed by I, slows down. The critical point is in the most elementary case at I=0.

However, the economically critical point may be reached earlier or later. The axiomatically correct macroeconomic Profit Law tells everyone that the point is reached earlier if, for example, the household sector’s saving Sm is greater than zero. The point is reached later if the government runs a deficit, i.e. if G−T is greater than zero.

The task of economic policy is to end economic growth before the physical limits are reached without destroying the economy by unknowingly switching from macroeconomic profit to loss. Needless to emphasize that economists have NO idea how to accomplish this feat. Walrasian, Keynesian, Marxian, and Austrian economics is proto-scientific garbage and therefore absolutely useless for economic policy.

The sad fate of humanity is: the (world-)economy will NOT break down for physical/ ecological reasons but because of the scientific incompetence a.k.a. stupidity of economists. How shabby an end compared to flood or fire.

Egmont Kakarot-Handtke

#1 For details of the big picture see cross-references Profit

Related 'Which breakdown?' and 'Mathematical Proof of the Breakdown of Capitalism' and 'Zero-sum capitalism' and 'Major Defects of the Market Economy' and 'Squaring the Investment Cycle'.

Obviously, you lack basic knowledge of the history of economic thought: “Late in life, moreover, he [Napoleon] claimed that he had always believed that if an empire were made of granite the ideas of economists if listened to, would suffice to reduce it to dust.” (Viner, 1963)

Nothing has changed since Napoleon. The stupidity of economists is as destructive as it ever was.#1, #2

#1 As Napoleon said: don’t listen to economists

#2 Economists and the destructive power of stupidity

You complain: “GDP and GDP growth has become the increasingly opaque lens through which we view society and ‘the economy.’ It is a cracked, scratched, smudged, distorting lens that may not even enable us to tell whether what we view through it is upside up or upside down.”

Fact is that economists have never gotten their foundational concepts straight and are too stupid for the elementary mathematics that underlies macroeconomics. The concept of GDP is a case in point.

For the axiomatically correct relationship between aggregate demand, investment, depreciation, productivity, price, income, and profit see Squaring the Investment Cycle.

Thank you for the information, the improved sentence reads: “The axiomatically correct macroeconomic Profit Law tells everyone that the [critical] point is reached earlier if, for example, the household sector’s saving Sm is greater than zero. The point is reached later if the government runs a deficit, i.e. if (G−T) is greater than zero.”

The beauty of this summary consists of answering the fundamental economic question: “... is the existing economic system in any significant sense self-adjusting.” (Keynes)

So, macrofounded economics tells everyone that microfounded equilibrium or steady-state models are a priori false and that the market system will eventually break down because of its built-in positive feedback mechanisms and NOT for sociological reasons, i.e. the revolution of the proletariat, or for ecological reasons, i.e. the limitedness of resources or the overabundance of pollution.

At the moment, the US economy runs already on life-support, i.e. on government deficit spending. Take it away and macroeconomic profit turns into macroeconomic loss and the economy breaks down. There is really no need for economists to calculate the “ … costs of abating carbon dioxide emissions and the long term future climate impacts from climate change.” (Newbold, Summary of the DICE model) because the economy as we know it has NO long-term future.#1

Economists should know how the economic system works but they don’t. For 150+ years, they waffle about supply-demand-equilibrium implying that the system regulates itself. This tenet is either self-deception or fraud or both. In any case, it catapults economists out of science.

#1 Mathematical Proof of the Breakdown of Capitalism

You say: “Dear Sandwichman welcome to the branch of Rabbit Hole Studies that is national statistics. :-)”

Economists know that science is about formal and material consistency: “Research is, in fact, a continuous discussion of the consistency of theories: formal consistency insofar as the discussion relates to the logical cohesion of what is asserted in joint theories; material consistency insofar as the agreement of observations with theories is concerned.” (Klant) Logical consistency is secured by applying the axiomatic-deductive method and empirical consistency is secured by applying state-of-art testing.

Economists know also that their proper business is political agenda pushing and NOT science. So, they deliberately try to keep everything in the swamp of vagueness and inconclusiveness because they know also: “Another thing I must point out is that you cannot prove a vague theory wrong.” (Feynman) This, of course, is the life insurance of failed/fake scientists.#1, #2

It is not an accident that economists apply concepts like utility, rational expectations, and aggregate real capital, which are obviously not measurable. And when the discussion comes to empirical testing, economists vanish through the jib door like the would-be gold makers of earlier times. The door bears the inscription ‘Measurement Problems’.

Political agenda pushers have learned this trick from priests.#3 The subject matter of priests is NONENTITIES. As J. S. Mill put it: “Mankind in all ages have had a strong propensity to conclude that wherever there is a name, there must be a distinguishable separate entity corresponding to the name; ...” This is the Fallacy of Reification.

The characteristic of economists is that they avoid well-defined concepts like the plague. Note that income, monetary profit, aggregate demand, and GDP can, in principle, be defined and measured with the precision of two decimal places but economists have managed to make a veritable mess of these foundational concepts.#4, #5

Economists advertise their stuff as science, well knowing that their theories/models are built upon NONENTITIES and that they will break down as soon as it comes to testing: “… suppose they did reject all theories that were empirically falsified ... Nothing would be left standing; there would be no economics.” (Hands)

National Statistics is NOT a Rabbit Hole but has been deliberately made a jib door through which failed/fake economists vanish when their proto-scientific fool’s gold is put to the acid test.#6, #7

#1 Postmodernism — the philosophy of scientific write-offs

#2 For details see cross-references Failed/Fake Scientists

#3 Wikipedia, Priest

#4 The Common Error of Common Sense: An Essential Rectification of the Accounting Approach

#5 Wikipedia and the promotion of economists’ idiotism

#6 Go! ― test the Profit and Employment Law

#7 Failed economics: The losers’ long list of lame excuses

You say: “… unfortunately I very strongly disagree that studies of the political economy can be a ‘science’ as in proper accuracy and falsification, in large part because experiments are difficult and repeatability is pretty rare, and never mind with the measurement problems, because the ‘Laws of Economics’ are not immutable, unless they are kept in ‘the swamp of vagueness and inconclusiveness’.”

Of course, you disagree. Take notice that your worn-out excuses have been refuted long ago.#1

According to its self-definition, economics is a science since Adam Smith/Karl Marx and this is celebrated once a year with the “Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel”.#2 So, economics has to be judged according to the well-known scientific standards of material/formal consistency.

Your fatal blunder is to maintain that economics is a social science while, in fact, it is a systems science.#3 And while there are no behavioral laws there are systemic laws.

Economists have not figured out these laws to this day. In fact, they are too stupid for the elementary mathematics that underlies macroeconomics.

Keynes’ scientific incompetence can be exactly located in the GT: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (p. 63)

Keynes got macroeconomic profit wrong: “His Collected Writings show that he wrestled to solve the Profit Puzzle up till the semi-final versions of his GT but in the end he gave up and discarded the draft chapter dealing with it.” (Tómasson et al.)

Let this sink in: the economist Keynes NEVER understood the foundational concept of his subject matter. Because profit is ill-defined the complete theoretical superstructure of Keynesianism is false. Keynesian policy guidance NEVER had valid scientific foundations. It has NEVER been anything else than political blather.

The elementary version of the axiomatically correct Profit Law, which is measurable with the precision of two decimal places, reads Qm≡I−Sm with Qm as monetary profit and Sm as monetary saving. And this means that since Keynes/Hicks ALL I=S/IS-LM models are false.#4 Macroeconomics is proto-scientific garbage. Microeconomics is even worse.

So after 80+ years of storytelling/blather, Keynesians, Post-Keynesians, Anti-Keynesians, New Keynesians, MMTers, Sandwichman, Blissex, and the rest of stupid/corrupt political agenda pushers together with all their peer-reviewed articles/textbooks/blog posts have finally to be flushed down the scientific toilet.

#1 Failed economics: The losers’ long list of lame excuses

#2 The real problem with the economics Nobel

#3 Economics is NOT a social science

#4 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

Blog-Reference

Ecological self-destruction is the subject matter of physics, biology, climatology, etcetera. Economists have nothing to say about these scientific issues because they are simply too incompetent for science. Economics is, after 200+ years, still at the proto-scientific level.

To make matters short, the central economic question is: Is the monetary economy sustainable on its own terms, that is, even if it faces no physical limits? The answer is NO.

Let us agree that, roughly speaking, the monetary economy as we know it can only exist if macroeconomic profit is positive and that the economy will break down if macroeconomic profit turns to loss. So, the question is, can it happen? and in case yes, when will it happen?

Now, the axiomatically correct macroeconomic Profit Law says Q≡Qm+Qn (i) with Qm≡Yd+(X−M)+(G−T)+(I−Sm) (ii) which simplifies to Qm≡I−Sm (iii) if Qn, Yd, X, M, G, T is set to zero.#1 Eq. (iii) says that monetary profit Qm is positive as long as the business sector’s investment expenditures are greater than the household sector’s saving. Or, if the household sector’s budget is balanced in each period, i.e. Sm=0 ⇒ Qm=I (iv), and this means that monetary profit Qm is positive as long as investment expenditures are positive (depreciation is a sub-item of Qn). In other words, the economy must grow or it drops dead. This may happen before the economy reaches the physical limits of growth.

The basic message of the Profit Law is that the monetary economy gets in trouble as soon as economic growth, expressed by I, slows down. The critical point is in the most elementary case at I=0.

However, the economically critical point may be reached earlier or later. The axiomatically correct macroeconomic Profit Law tells everyone that the point is reached earlier if, for example, the household sector’s saving Sm is greater than zero. The point is reached later if the government runs a deficit, i.e. if G−T is greater than zero.

The task of economic policy is to end economic growth before the physical limits are reached without destroying the economy by unknowingly switching from macroeconomic profit to loss. Needless to emphasize that economists have NO idea how to accomplish this feat. Walrasian, Keynesian, Marxian, and Austrian economics is proto-scientific garbage and therefore absolutely useless for economic policy.

The sad fate of humanity is: the (world-)economy will NOT break down for physical/ ecological reasons but because of the scientific incompetence a.k.a. stupidity of economists. How shabby an end compared to flood or fire.

Egmont Kakarot-Handtke

#1 For details of the big picture see cross-references Profit

Related 'Which breakdown?' and 'Mathematical Proof of the Breakdown of Capitalism' and 'Zero-sum capitalism' and 'Major Defects of the Market Economy' and 'Squaring the Investment Cycle'.

***

REPLY to Anonymous on Nov 1Obviously, you lack basic knowledge of the history of economic thought: “Late in life, moreover, he [Napoleon] claimed that he had always believed that if an empire were made of granite the ideas of economists if listened to, would suffice to reduce it to dust.” (Viner, 1963)

Nothing has changed since Napoleon. The stupidity of economists is as destructive as it ever was.#1, #2

#1 As Napoleon said: don’t listen to economists

#2 Economists and the destructive power of stupidity

***

REPLY to Sandwichman on Nov 1You complain: “GDP and GDP growth has become the increasingly opaque lens through which we view society and ‘the economy.’ It is a cracked, scratched, smudged, distorting lens that may not even enable us to tell whether what we view through it is upside up or upside down.”

Fact is that economists have never gotten their foundational concepts straight and are too stupid for the elementary mathematics that underlies macroeconomics. The concept of GDP is a case in point.

For the axiomatically correct relationship between aggregate demand, investment, depreciation, productivity, price, income, and profit see Squaring the Investment Cycle.

***

REPLY to Barkley Rosser, Sandwichman on Nov 2Thank you for the information, the improved sentence reads: “The axiomatically correct macroeconomic Profit Law tells everyone that the [critical] point is reached earlier if, for example, the household sector’s saving Sm is greater than zero. The point is reached later if the government runs a deficit, i.e. if (G−T) is greater than zero.”

The beauty of this summary consists of answering the fundamental economic question: “... is the existing economic system in any significant sense self-adjusting.” (Keynes)

So, macrofounded economics tells everyone that microfounded equilibrium or steady-state models are a priori false and that the market system will eventually break down because of its built-in positive feedback mechanisms and NOT for sociological reasons, i.e. the revolution of the proletariat, or for ecological reasons, i.e. the limitedness of resources or the overabundance of pollution.

At the moment, the US economy runs already on life-support, i.e. on government deficit spending. Take it away and macroeconomic profit turns into macroeconomic loss and the economy breaks down. There is really no need for economists to calculate the “ … costs of abating carbon dioxide emissions and the long term future climate impacts from climate change.” (Newbold, Summary of the DICE model) because the economy as we know it has NO long-term future.#1

Economists should know how the economic system works but they don’t. For 150+ years, they waffle about supply-demand-equilibrium implying that the system regulates itself. This tenet is either self-deception or fraud or both. In any case, it catapults economists out of science.

#1 Mathematical Proof of the Breakdown of Capitalism

***

REPLY to Blissex on Nov 4You say: “Dear Sandwichman welcome to the branch of Rabbit Hole Studies that is national statistics. :-)”

Economists know that science is about formal and material consistency: “Research is, in fact, a continuous discussion of the consistency of theories: formal consistency insofar as the discussion relates to the logical cohesion of what is asserted in joint theories; material consistency insofar as the agreement of observations with theories is concerned.” (Klant) Logical consistency is secured by applying the axiomatic-deductive method and empirical consistency is secured by applying state-of-art testing.

Economists know also that their proper business is political agenda pushing and NOT science. So, they deliberately try to keep everything in the swamp of vagueness and inconclusiveness because they know also: “Another thing I must point out is that you cannot prove a vague theory wrong.” (Feynman) This, of course, is the life insurance of failed/fake scientists.#1, #2

It is not an accident that economists apply concepts like utility, rational expectations, and aggregate real capital, which are obviously not measurable. And when the discussion comes to empirical testing, economists vanish through the jib door like the would-be gold makers of earlier times. The door bears the inscription ‘Measurement Problems’.

Political agenda pushers have learned this trick from priests.#3 The subject matter of priests is NONENTITIES. As J. S. Mill put it: “Mankind in all ages have had a strong propensity to conclude that wherever there is a name, there must be a distinguishable separate entity corresponding to the name; ...” This is the Fallacy of Reification.

The characteristic of economists is that they avoid well-defined concepts like the plague. Note that income, monetary profit, aggregate demand, and GDP can, in principle, be defined and measured with the precision of two decimal places but economists have managed to make a veritable mess of these foundational concepts.#4, #5

Economists advertise their stuff as science, well knowing that their theories/models are built upon NONENTITIES and that they will break down as soon as it comes to testing: “… suppose they did reject all theories that were empirically falsified ... Nothing would be left standing; there would be no economics.” (Hands)

National Statistics is NOT a Rabbit Hole but has been deliberately made a jib door through which failed/fake economists vanish when their proto-scientific fool’s gold is put to the acid test.#6, #7

#1 Postmodernism — the philosophy of scientific write-offs

#2 For details see cross-references Failed/Fake Scientists

#3 Wikipedia, Priest

#4 The Common Error of Common Sense: An Essential Rectification of the Accounting Approach

#5 Wikipedia and the promotion of economists’ idiotism

#6 Go! ― test the Profit and Employment Law

#7 Failed economics: The losers’ long list of lame excuses

***

REPLY to Blissex on Nov 6You say: “… unfortunately I very strongly disagree that studies of the political economy can be a ‘science’ as in proper accuracy and falsification, in large part because experiments are difficult and repeatability is pretty rare, and never mind with the measurement problems, because the ‘Laws of Economics’ are not immutable, unless they are kept in ‘the swamp of vagueness and inconclusiveness’.”

Of course, you disagree. Take notice that your worn-out excuses have been refuted long ago.#1

According to its self-definition, economics is a science since Adam Smith/Karl Marx and this is celebrated once a year with the “Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel”.#2 So, economics has to be judged according to the well-known scientific standards of material/formal consistency.

Your fatal blunder is to maintain that economics is a social science while, in fact, it is a systems science.#3 And while there are no behavioral laws there are systemic laws.

Economists have not figured out these laws to this day. In fact, they are too stupid for the elementary mathematics that underlies macroeconomics.

Keynes’ scientific incompetence can be exactly located in the GT: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (p. 63)

Keynes got macroeconomic profit wrong: “His Collected Writings show that he wrestled to solve the Profit Puzzle up till the semi-final versions of his GT but in the end he gave up and discarded the draft chapter dealing with it.” (Tómasson et al.)

Let this sink in: the economist Keynes NEVER understood the foundational concept of his subject matter. Because profit is ill-defined the complete theoretical superstructure of Keynesianism is false. Keynesian policy guidance NEVER had valid scientific foundations. It has NEVER been anything else than political blather.

The elementary version of the axiomatically correct Profit Law, which is measurable with the precision of two decimal places, reads Qm≡I−Sm with Qm as monetary profit and Sm as monetary saving. And this means that since Keynes/Hicks ALL I=S/IS-LM models are false.#4 Macroeconomics is proto-scientific garbage. Microeconomics is even worse.

So after 80+ years of storytelling/blather, Keynesians, Post-Keynesians, Anti-Keynesians, New Keynesians, MMTers, Sandwichman, Blissex, and the rest of stupid/corrupt political agenda pushers together with all their peer-reviewed articles/textbooks/blog posts have finally to be flushed down the scientific toilet.

#1 Failed economics: The losers’ long list of lame excuses

#2 The real problem with the economics Nobel

#3 Economics is NOT a social science

#4 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

August 30, 2017

Keynesians ― terminally stupid or worse?

Comment on Dirk Ehnts on ‘Keynes on Savings and Investment’

Blog-Reference and Blog-Reference

Eighty years ago, Keynes got macro wrong and Keynesians did not notice it until this very day.

Dirk Ehnts cites Keynes: “S=I at all rates of investment.” and comments enthusiastically: “This is very enlightening. The ‘General Theory’ also contained the issue of savings and investment, but the quote above nails it. There is no ‘supply’ and ‘demand’ for capital, hence savings and investment do not need anything to move so that there can be equilibrium.”

There is no better proof of the abysmal scientific incompetence of economists in general and of Keynesians in particular than S=I.

Here is the evidence from the General Theory: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (p. 63)

This syllogism is conceptually and logically defective because Keynes did not come to grips with profit. “His Collected Writings show that he wrestled to solve the Profit Puzzle up till the semi-final versions of his GT but in the end he gave up and discarded the draft chapter dealing with it.” (Tómasson et al.)

Because profit is ill-defined the whole theoretical superstructure of Keynesianism is false.#1 Let this sink in: Keynes had NO idea of the fundamental concepts of economics, viz. profit and income. Keynes, though, was not alone: “... one of the most convoluted and muddled areas in economic theory: the theory of profit.” (Mirowski) The fact is, the profit theory is false since Adam Smith. Economics is scientifically worthless for 200+ years.

What has to be done is to replace Keynes’ false macrofoundations with true macrofoundations. The elemenatry production-consumption economy is, for a start, defined by three macro axioms (Yw=WL, O=RL, C=PX), two conditions (X=O, C=Yw), and two definitions (monetary profit Qm≡C−Yw, monetary saving Sm≡Yw−C). The graphical representation is shown on Wikimedia.#2, #3

It always holds Qm≡−Sm, in other words, at the heart of the monetary economy is an identity: The business sector’s deficit equals the household sector’s surplus and vice versa. Put bluntly, the business sector's loss is the counterpart of the household sector's saving and vice versa profit is the counterpart of dissaving. This is the most elementary form of the macroeconomic Profit Law. It follows directly from the definition of the business sector’s monetary profit Qm≡C−Yw and the definition of the household sector’s monetary saving Sm≡Yw−C. From this immediately follows that Keynes’ foundational identity “Income = value of output” is false and After-Keynesians have not realized it to this day.

For the investment economy, the Profit Law reads Qm≡I−Sm. Legend: Qm monetary profit, I investment expenditures, Sm monetary saving/dissaving. The business sector’s investment expenditures and the household sector’s saving/dissaving are completely INDEPENDENT and NEVER equal.

There is NO such thing as equality of investment and saving, neither ex-ante nor ex-post, and there is NO such thing as an equilibrium of I and S. Keynes was too stupid to understand this, and After-Keynesians are even worse.#4

Egmont Kakarot-Handtke

#1 Why Post Keynesianism Is Not Yet a Science

#2 Wikimedia AXEC31 The elementary production-consumption economy

#3 How the intelligent non-economist can refute every economist hands down

#4 For details of the big picture see cross-references Refutation of I=S and cross-references Keynesianism.

You say: “I don’t understand your claim because it comes without any argument.”

The proof has been given that Qm≡−Sm in the pure production-consumption economy and Qm≡I−Sm in the elementary investment economy. In plain text, the proof says that saving and investment are NEVER equal.#1

You say: “Regarding wording, how about: ‘saving is the accounting record of investment’? I find it immensely useful!”

In their pathetic incompetence, economists got even the elementary mathematics of accounting wrong.#2 The wording ‘saving is the accounting record of investment’ is the very proof that economists cannot even put 2 and 2 together.

You say: “What I don’t find useful is the inclusion of profits in macroeconomic models.”

Macroeconomic profit exists and economists should know and tell what it is. Neither orthodox nor heterodox economists do it, though, because they have no idea what the pivotal concept of their subject matter is.#3

You say: “Of course, the question of what drives investment needs to be attacked using the concept of profit, but that is a different question from what determines the level of unemployment, which was Keynes’ question in the GT!”

Keynes’ employment theory is false because I=S ― and, by implication, the multiplier ― is false which, in turn, is false because Keynes never understood what profit is.#4

Because Keynes’ premise Income = value of output is false, ALL I=S/IS-LM models from Keynes/Hicks to Krugman/Ehnts are provably false.#5, #6

After-Keynesians are light years behind the curve. The scientific level of economists in general and Dirk Ehnts, in particular, is worse than zero.

#1 How Keynes got macro wrong and Allais got it right and

The Three Fatal Mistakes of Yesterday Economics: Profit, I=S, Employment

#2 A tale of three accountants and cross-references Accounting

#3 Heterodoxy, too, is proto-scientific garbage

#4 Keynes’ Employment Function and the Gratuitous Phillips Curve Disaster

#5 Getting out of IS-LM = Getting out of despair

#6 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

Dirk Ehnts subscribes to: “S = I at all rates of investment. Y either definable as C+S or as C+I. S and I were opposite facets of the same phenomenon they did not need a rate of interest to bring them into equilibrium for they were at all times and in all conditions in equilibrium.”

Nick Edmonds maintains: “The expected real rate of interest is in some sense the price of savings and so, in principle, changes in this expected rate might be able to reconcile desired saving and desired investment. In a barter economy, goods for current delivery can be traded for promises of the same goods for future delivery.”

Keynes was right on two points: (i) he has to be credited for realizing that the economics of Jevons/Walras/Menger/Marshall was false at its core and that nothing less than a paradigm shift was needed, (ii) that economic analysis has to start with the ‘monetary theory of production’ and NOT with some silly barter economy of the Sraffa type.#1

From the analysis of the most elementary economic configuration, the pure production-consumption economy, follows for the balances Qm≡−Sm, in other words, at the heart of the monetary economy is an identity: the business sector’s deficit = loss (surplus = profit) equals the household sector’s surplus = saving (deficit = dissaving). Loss is the counterpart of saving and profit is the counterpart of dissaving. This is the most elementary form of the macroeconomic Profit Law.#2

This, first of all, tells one that the profit theory is false since Smith and Ricardo.#3 And, secondly, this tells one that the theory of saving and investment is false by implication. It always holds Qm≡I−Sm, that is, investment and saving are NEVER equal, neither in accounting nor in reality.#4

All I=S/IS-LM models are provably false from Wicksell/Keynes/Hicks onward. Because MMT is built upon the false Keynesian balances equations it is false, too.#5

#1 The futile attempt to recycle Sraffa

#2 How the intelligent non-economist can refute every economist hands down

#3 When Ricardo Saw Profit, He Called It Rent: On the Vice of Parochial Realism

#4 Rectification of MMT macro accounting

#5 For the full-spectrum refutation of MMT see cross-references MMT

Blog-Reference and Blog-Reference

Eighty years ago, Keynes got macro wrong and Keynesians did not notice it until this very day.

Dirk Ehnts cites Keynes: “S=I at all rates of investment.” and comments enthusiastically: “This is very enlightening. The ‘General Theory’ also contained the issue of savings and investment, but the quote above nails it. There is no ‘supply’ and ‘demand’ for capital, hence savings and investment do not need anything to move so that there can be equilibrium.”

There is no better proof of the abysmal scientific incompetence of economists in general and of Keynesians in particular than S=I.

Here is the evidence from the General Theory: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (p. 63)

This syllogism is conceptually and logically defective because Keynes did not come to grips with profit. “His Collected Writings show that he wrestled to solve the Profit Puzzle up till the semi-final versions of his GT but in the end he gave up and discarded the draft chapter dealing with it.” (Tómasson et al.)

Because profit is ill-defined the whole theoretical superstructure of Keynesianism is false.#1 Let this sink in: Keynes had NO idea of the fundamental concepts of economics, viz. profit and income. Keynes, though, was not alone: “... one of the most convoluted and muddled areas in economic theory: the theory of profit.” (Mirowski) The fact is, the profit theory is false since Adam Smith. Economics is scientifically worthless for 200+ years.

What has to be done is to replace Keynes’ false macrofoundations with true macrofoundations. The elemenatry production-consumption economy is, for a start, defined by three macro axioms (Yw=WL, O=RL, C=PX), two conditions (X=O, C=Yw), and two definitions (monetary profit Qm≡C−Yw, monetary saving Sm≡Yw−C). The graphical representation is shown on Wikimedia.#2, #3

For the investment economy, the Profit Law reads Qm≡I−Sm. Legend: Qm monetary profit, I investment expenditures, Sm monetary saving/dissaving. The business sector’s investment expenditures and the household sector’s saving/dissaving are completely INDEPENDENT and NEVER equal.

There is NO such thing as equality of investment and saving, neither ex-ante nor ex-post, and there is NO such thing as an equilibrium of I and S. Keynes was too stupid to understand this, and After-Keynesians are even worse.#4

Egmont Kakarot-Handtke

#1 Why Post Keynesianism Is Not Yet a Science

#2 Wikimedia AXEC31 The elementary production-consumption economy

#3 How the intelligent non-economist can refute every economist hands down

#4 For details of the big picture see cross-references Refutation of I=S and cross-references Keynesianism.

***

REPLY to Dirk Ehnts on Sep 1,3 see also hereYou say: “I don’t understand your claim because it comes without any argument.”

The proof has been given that Qm≡−Sm in the pure production-consumption economy and Qm≡I−Sm in the elementary investment economy. In plain text, the proof says that saving and investment are NEVER equal.#1

You say: “Regarding wording, how about: ‘saving is the accounting record of investment’? I find it immensely useful!”

In their pathetic incompetence, economists got even the elementary mathematics of accounting wrong.#2 The wording ‘saving is the accounting record of investment’ is the very proof that economists cannot even put 2 and 2 together.

You say: “What I don’t find useful is the inclusion of profits in macroeconomic models.”

Macroeconomic profit exists and economists should know and tell what it is. Neither orthodox nor heterodox economists do it, though, because they have no idea what the pivotal concept of their subject matter is.#3

You say: “Of course, the question of what drives investment needs to be attacked using the concept of profit, but that is a different question from what determines the level of unemployment, which was Keynes’ question in the GT!”

Keynes’ employment theory is false because I=S ― and, by implication, the multiplier ― is false which, in turn, is false because Keynes never understood what profit is.#4

Because Keynes’ premise Income = value of output is false, ALL I=S/IS-LM models from Keynes/Hicks to Krugman/Ehnts are provably false.#5, #6

After-Keynesians are light years behind the curve. The scientific level of economists in general and Dirk Ehnts, in particular, is worse than zero.

#1 How Keynes got macro wrong and Allais got it right and

The Three Fatal Mistakes of Yesterday Economics: Profit, I=S, Employment

#2 A tale of three accountants and cross-references Accounting

#3 Heterodoxy, too, is proto-scientific garbage

#4 Keynes’ Employment Function and the Gratuitous Phillips Curve Disaster

#5 Getting out of IS-LM = Getting out of despair

#6 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

***

Wikimedia AXEC172

***

COMMENT on Nick Edmonds, Dirk Ehnts on Sep 5, see also hereDirk Ehnts subscribes to: “S = I at all rates of investment. Y either definable as C+S or as C+I. S and I were opposite facets of the same phenomenon they did not need a rate of interest to bring them into equilibrium for they were at all times and in all conditions in equilibrium.”

Nick Edmonds maintains: “The expected real rate of interest is in some sense the price of savings and so, in principle, changes in this expected rate might be able to reconcile desired saving and desired investment. In a barter economy, goods for current delivery can be traded for promises of the same goods for future delivery.”

Keynes was right on two points: (i) he has to be credited for realizing that the economics of Jevons/Walras/Menger/Marshall was false at its core and that nothing less than a paradigm shift was needed, (ii) that economic analysis has to start with the ‘monetary theory of production’ and NOT with some silly barter economy of the Sraffa type.#1

From the analysis of the most elementary economic configuration, the pure production-consumption economy, follows for the balances Qm≡−Sm, in other words, at the heart of the monetary economy is an identity: the business sector’s deficit = loss (surplus = profit) equals the household sector’s surplus = saving (deficit = dissaving). Loss is the counterpart of saving and profit is the counterpart of dissaving. This is the most elementary form of the macroeconomic Profit Law.#2

This, first of all, tells one that the profit theory is false since Smith and Ricardo.#3 And, secondly, this tells one that the theory of saving and investment is false by implication. It always holds Qm≡I−Sm, that is, investment and saving are NEVER equal, neither in accounting nor in reality.#4

All I=S/IS-LM models are provably false from Wicksell/Keynes/Hicks onward. Because MMT is built upon the false Keynesian balances equations it is false, too.#5

#1 The futile attempt to recycle Sraffa

#2 How the intelligent non-economist can refute every economist hands down

#3 When Ricardo Saw Profit, He Called It Rent: On the Vice of Parochial Realism

#4 Rectification of MMT macro accounting

#5 For the full-spectrum refutation of MMT see cross-references MMT

August 10, 2017

Sending Solow’s growth model to the dump of proto-scientific history

Comment on Luis C. Corchón on ‘A Malthus-Swan Model of Economic Growth’

Blog-Reference

Economics fits Feynman’s definition of a cargo cult science “They’re doing everything right. The form is perfect. ... But it doesn’t work. ... So I call these things cargo cult science because they follow all the apparent precepts and forms of scientific investigation, but they’re missing something essential.”

Orthodox economics messed up the theory of production. Georgescu-Roegen was quite clear about “… the completely faulty form by which standard economics represents a production process”. As a consequence, all growth models of the Solow-type since the QJE paper of 1956 are worthless. But the problem goes deeper. ALL microfounded models are worthless.

The whole theoretical superstructure of Orthodoxy is based upon this set of hardcore propositions a.k.a. axioms: “HC1 economic agents have preferences over outcomes; HC2 agents individually optimize subject to constraints; HC3 agent choice is manifest in interrelated markets; HC4 agents have full relevant knowledge; HC5 observable outcomes are coordinated, and must be discussed with reference to equilibrium states.” (Weintraub)

In order to be applicable HC2, which translates formally into calculus, requires a lot of auxiliary assumptions, most prominently a well-behaved production function. The compelling reason for the introduction of out-of-thin-air auxiliary assumptions is that without these specifications the axiom HC2 does NOT work and the whole of Marginalism, which hinges on HC2, falls apart.

It should be pretty obvious that the axiomatic core of Orthodoxy contains THREE NONENTITIES: (i) constrained optimization HC2, (ii) rational expectations HC4, (iii) equilibrium HC5. Every theory/model that contains a NONENTITY is a priori false. This includes all Solow-type models.

Economics has to start — NOT with behavioral assumptions — but with the ‘monetary theory of production’ (Keynes). The elementary production-consumption economy is defined with systemic (= behavior-free) axioms: (A0) The objectively given and most elementary configuration of the economy consists of the household and the business sector which in turn consists initially of one giant fully integrated firm. (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

These premises are certain, true, and primary, and therefore satisfy all methodological requirements. The set of premises is minimal, that is, it cannot be reduced further, only expanded. The set contains no nonentities like maximization or equilibrium and no normative assertions. Note that all variables are measurable.

For a start, it holds market-clearing X=O and budget-balancing C=Yw.

Monetary profit is defined as Qm≡C−Yw and monetary saving is defined as Sm≡Yw−C. It always holds Qm≡−Sm, which is the most elementary form of the macroeconomic Profit Law.

Under the conditions of market-clearing and budget-balancing in each period, the price follows as P=W/R, i.e. the market-clearing price is equal to unit wage costs. This is the most elementary form of the macroeconomic Law of Supply and Demand. It translates into W/P=R, i.e. the real wage is equal to the productivity.

The changes in the wage rate from period to period are formally given by Wt=Wt-1(1+wt). Analogous for all other independent variables. The rates of change for future periods are, for a start, taken to be random variables.

With this, the formal framework of the elementary growth model for the elementary production-consumption economy is defined. The systemic formal framework#2, which combines the nominal and real key variables, fully replaces all Solow-type real models.

It does not matter how employment develops, that is, whether the labor force grows or shrinks over time. If the productivity remains constant with growing (shrinking) employment the real wage does not change. If productivity increases, so does the real wage. Labor gets always its full product. Monetary profit is zero. If the productivity declines the real wage heads towards the subsistence level. This, though, has nothing to do with exploitation. Needless to say at the subsistence level, all further expansion comes to a halt. This is the Malthusian outcome. The ultimate driver of real affluence is increasing returns.

This was the first step. In the second step investment and capital have to be added.#3

Egmont Kakarot-Handtke

#1 The future of economics: why you will probably not be admitted to it, and why this is a good thing

#2 The Economics God Equation (including distribution) is shown on Wikimedia AXEC25

For this equation Computational Irreducibility in the sense of Stephen Wolfram, A New Kind of Science, Wolfram Media, 1959, pp. 737 ff. holds.

#3 Squaring the Investment Cycle

Related 'Saving NEVER equals investment' and 'Is Nick Rowe stupid or corrupt or both?' and 'Macro for dummies' and 'Do first your macroeconomic homework!' and 'Settling the Theory of Saving' and 'Solow and the ludicrousness of economics' and 'Robert Solow and Lars Syll, fake scientists' and 'Solow and the ludicrousness of economics' and 'The moral of the story' and 'No future for the representative economist' and 'All economists together now: Solow’s Swan Song' and 'When substandard thinkers dabble in science it is called economics' and 'When substandard thinkers dabble in science it is called economics' and 'High profits and low economics' For details of the big picture see cross-references Failed/Fake Scientists and cross-references Paradigm Shift and cross-references Refutation of I=S.

Blog-Reference

Economics fits Feynman’s definition of a cargo cult science “They’re doing everything right. The form is perfect. ... But it doesn’t work. ... So I call these things cargo cult science because they follow all the apparent precepts and forms of scientific investigation, but they’re missing something essential.”

Orthodox economics messed up the theory of production. Georgescu-Roegen was quite clear about “… the completely faulty form by which standard economics represents a production process”. As a consequence, all growth models of the Solow-type since the QJE paper of 1956 are worthless. But the problem goes deeper. ALL microfounded models are worthless.

The whole theoretical superstructure of Orthodoxy is based upon this set of hardcore propositions a.k.a. axioms: “HC1 economic agents have preferences over outcomes; HC2 agents individually optimize subject to constraints; HC3 agent choice is manifest in interrelated markets; HC4 agents have full relevant knowledge; HC5 observable outcomes are coordinated, and must be discussed with reference to equilibrium states.” (Weintraub)

In order to be applicable HC2, which translates formally into calculus, requires a lot of auxiliary assumptions, most prominently a well-behaved production function. The compelling reason for the introduction of out-of-thin-air auxiliary assumptions is that without these specifications the axiom HC2 does NOT work and the whole of Marginalism, which hinges on HC2, falls apart.

It should be pretty obvious that the axiomatic core of Orthodoxy contains THREE NONENTITIES: (i) constrained optimization HC2, (ii) rational expectations HC4, (iii) equilibrium HC5. Every theory/model that contains a NONENTITY is a priori false. This includes all Solow-type models.

Economics has to start — NOT with behavioral assumptions — but with the ‘monetary theory of production’ (Keynes). The elementary production-consumption economy is defined with systemic (= behavior-free) axioms: (A0) The objectively given and most elementary configuration of the economy consists of the household and the business sector which in turn consists initially of one giant fully integrated firm. (A1) Yw=WL wage income Yw is equal to wage rate W times working hours. L, (A2) O=RL output O is equal to productivity R times working hours L, (A3) C=PX consumption expenditure C is equal to price P times quantity bought/sold X.

These premises are certain, true, and primary, and therefore satisfy all methodological requirements. The set of premises is minimal, that is, it cannot be reduced further, only expanded. The set contains no nonentities like maximization or equilibrium and no normative assertions. Note that all variables are measurable.

For a start, it holds market-clearing X=O and budget-balancing C=Yw.

Monetary profit is defined as Qm≡C−Yw and monetary saving is defined as Sm≡Yw−C. It always holds Qm≡−Sm, which is the most elementary form of the macroeconomic Profit Law.

Under the conditions of market-clearing and budget-balancing in each period, the price follows as P=W/R, i.e. the market-clearing price is equal to unit wage costs. This is the most elementary form of the macroeconomic Law of Supply and Demand. It translates into W/P=R, i.e. the real wage is equal to the productivity.

The changes in the wage rate from period to period are formally given by Wt=Wt-1(1+wt). Analogous for all other independent variables. The rates of change for future periods are, for a start, taken to be random variables.

With this, the formal framework of the elementary growth model for the elementary production-consumption economy is defined. The systemic formal framework#2, which combines the nominal and real key variables, fully replaces all Solow-type real models.

It does not matter how employment develops, that is, whether the labor force grows or shrinks over time. If the productivity remains constant with growing (shrinking) employment the real wage does not change. If productivity increases, so does the real wage. Labor gets always its full product. Monetary profit is zero. If the productivity declines the real wage heads towards the subsistence level. This, though, has nothing to do with exploitation. Needless to say at the subsistence level, all further expansion comes to a halt. This is the Malthusian outcome. The ultimate driver of real affluence is increasing returns.

This was the first step. In the second step investment and capital have to be added.#3

Egmont Kakarot-Handtke

#1 The future of economics: why you will probably not be admitted to it, and why this is a good thing

#2 The Economics God Equation (including distribution) is shown on Wikimedia AXEC25

|

| The Economics God Equation ® |

For this equation Computational Irreducibility in the sense of Stephen Wolfram, A New Kind of Science, Wolfram Media, 1959, pp. 737 ff. holds.

Related 'Saving NEVER equals investment' and 'Is Nick Rowe stupid or corrupt or both?' and 'Macro for dummies' and 'Do first your macroeconomic homework!' and 'Settling the Theory of Saving' and 'Solow and the ludicrousness of economics' and 'Robert Solow and Lars Syll, fake scientists' and 'Solow and the ludicrousness of economics' and 'The moral of the story' and 'No future for the representative economist' and 'All economists together now: Solow’s Swan Song' and 'When substandard thinkers dabble in science it is called economics' and 'When substandard thinkers dabble in science it is called economics' and 'High profits and low economics' For details of the big picture see cross-references Failed/Fake Scientists and cross-references Paradigm Shift and cross-references Refutation of I=S.

Loanable funds ― no hoax, just breathtaking stupidity

Comment on Lars Syll on ‘The loanable funds hoax’

Blog-Reference and Blog-Reference and Blog-Reference on Aug 12

Lars Syll states: “In the traditional loanable funds theory — as presented in mainstream macroeconomics textbooks — the amount of loans and credit available for financing investment is constrained by how much saving is available. Saving is the supply of loanable funds, investment is the demand for loanable funds and assumed to be negatively related to the interest rate. Lowering households’ consumption means increasing savings via a lower interest. That view has been shown to have very little to do with reality. It’s nothing but an otherworldly neoclassical fantasy.”

This, of course, is true. Anytime an economist paints supply-curve—demand-curve—equilibrium it is proto-scientific garbage, no matter what is written on the axes.#1 The standard analytical tool, i.e. SS-curve―DD-curve―intersection, represents a NONENTITY. By consequence, any supply-demand-equilibrium discussion is as senseless as any dancing-angels-on-a-pinpoint discussion.

Lars Syll’s critique of the loanable funds theory is correct on all scores. The problem, though, is that BOTH orthodox and heterodox economists are scientifically incompetent. The proof is in the fact that heterodox alternatives are regularly just as crappy as the orthodox original. They look only different at the surface level.

Lars Syll quotes Kalecki approvingly: “It should be emphasized that the equality between savings and investment … will be valid under all circumstances. In particular, it will be independent of the level of the rate of interest which was customarily considered in economic theory to be the factor equilibrating the demand for and supply of new capital.”

Kalecki, of course, is wrong. Saving and investment are NEVER equal, neither ex-ante nor ex-post. Keynes, of course, got it also wrong: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (GT, p. 63)

In order to prove this, one has to go back to the basics of what Keynes called ‘the monetary theory of production’. The pure production-consumption economy is for a start defined by three macro axioms (Yw=WL, O=RL, C=PX), two conditions (X=O, C=Yw), and two definitions (monetary profit Qm≡C−Yw, monetary saving Sm≡Yw−C).#2

It always holds Qm≡−Sm, in other words, the business sector’s deficit (surplus) equals the household sector’s surplus (deficit). Loss is the counterpart of saving and profit is the counterpart of dissaving. This is the most elementary form of the macroeconomic Profit Law. It implies that saving and investment are NOT equal, simply because there is no investment in the pure consumption economy but there is saving/dissaving.#3

So, Kalecki is refuted, Keynes is refuted, and all the rest of the IS-LM crowd up to Krugman is refuted.#4

For the investment economy holds Qm=I−Sm. The DIFFERENCE between investment and saving, which exists at ANY moment on the time axis determines monetary profit Qm, which is measurable with the precision of two decimal places.

The orthodox loanable funds theory is false but the heterodox alternatives are also false. Economists are too stupid for elementary algebra.#5 This is NOT a hoax, this is real.#6

Egmont Kakarot-Handtke

#1 There is NO such thing as supply-demand-equilibrium

#2 The tiny little problem with economics

#3 See also ‘Macro for dummies’

#4 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

#5 Economists: just too stupid for counting

#6 Fact of life: your econ prof is scientifically incompetent

Related 'Fixing the loanable funds blunder'. For details of the big picture see cross-references Refutation of I=S

Blog-Reference and Blog-Reference and Blog-Reference on Aug 12

Lars Syll states: “In the traditional loanable funds theory — as presented in mainstream macroeconomics textbooks — the amount of loans and credit available for financing investment is constrained by how much saving is available. Saving is the supply of loanable funds, investment is the demand for loanable funds and assumed to be negatively related to the interest rate. Lowering households’ consumption means increasing savings via a lower interest. That view has been shown to have very little to do with reality. It’s nothing but an otherworldly neoclassical fantasy.”

This, of course, is true. Anytime an economist paints supply-curve—demand-curve—equilibrium it is proto-scientific garbage, no matter what is written on the axes.#1 The standard analytical tool, i.e. SS-curve―DD-curve―intersection, represents a NONENTITY. By consequence, any supply-demand-equilibrium discussion is as senseless as any dancing-angels-on-a-pinpoint discussion.

Lars Syll’s critique of the loanable funds theory is correct on all scores. The problem, though, is that BOTH orthodox and heterodox economists are scientifically incompetent. The proof is in the fact that heterodox alternatives are regularly just as crappy as the orthodox original. They look only different at the surface level.

Lars Syll quotes Kalecki approvingly: “It should be emphasized that the equality between savings and investment … will be valid under all circumstances. In particular, it will be independent of the level of the rate of interest which was customarily considered in economic theory to be the factor equilibrating the demand for and supply of new capital.”

Kalecki, of course, is wrong. Saving and investment are NEVER equal, neither ex-ante nor ex-post. Keynes, of course, got it also wrong: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (GT, p. 63)

In order to prove this, one has to go back to the basics of what Keynes called ‘the monetary theory of production’. The pure production-consumption economy is for a start defined by three macro axioms (Yw=WL, O=RL, C=PX), two conditions (X=O, C=Yw), and two definitions (monetary profit Qm≡C−Yw, monetary saving Sm≡Yw−C).#2

It always holds Qm≡−Sm, in other words, the business sector’s deficit (surplus) equals the household sector’s surplus (deficit). Loss is the counterpart of saving and profit is the counterpart of dissaving. This is the most elementary form of the macroeconomic Profit Law. It implies that saving and investment are NOT equal, simply because there is no investment in the pure consumption economy but there is saving/dissaving.#3

So, Kalecki is refuted, Keynes is refuted, and all the rest of the IS-LM crowd up to Krugman is refuted.#4

For the investment economy holds Qm=I−Sm. The DIFFERENCE between investment and saving, which exists at ANY moment on the time axis determines monetary profit Qm, which is measurable with the precision of two decimal places.

The orthodox loanable funds theory is false but the heterodox alternatives are also false. Economists are too stupid for elementary algebra.#5 This is NOT a hoax, this is real.#6

Egmont Kakarot-Handtke

#1 There is NO such thing as supply-demand-equilibrium

#2 The tiny little problem with economics

#3 See also ‘Macro for dummies’

#4 Mr. Keynes, Prof. Krugman, IS-LM, and the End of Economics as We Know It

#5 Economists: just too stupid for counting

#6 Fact of life: your econ prof is scientifically incompetent

Related 'Fixing the loanable funds blunder'. For details of the big picture see cross-references Refutation of I=S

December 30, 2016

Let Keynes rest in peace

Comment on Koichi Hamada on ‘Keynes Reborn’

Blog-Reference and Blog-Reference

Walrasian, Keynesian, Marxian, and Austrian economists are groping in the dark with regard to the two most important features of the market economy, that is, the profit mechanism and the price mechanism. To get out of failed economic theory requires nothing less than a full-blown paradigm shift.

In the following, a sketch of the correct employment theory is given.#1 The most elementary version of the objective systemic Employment Law is shown on Wikimedia AXEC62:

#1 For details see The Three Fatal Mistakes of Yesterday Economics: Profit, I=S, Employment.

Blog-Reference and Blog-Reference

Walrasian, Keynesian, Marxian, and Austrian economists are groping in the dark with regard to the two most important features of the market economy, that is, the profit mechanism and the price mechanism. To get out of failed economic theory requires nothing less than a full-blown paradigm shift.

In the following, a sketch of the correct employment theory is given.#1 The most elementary version of the objective systemic Employment Law is shown on Wikimedia AXEC62:

From this equation follows:

(i) An increase in the expenditure ratio ρE leads to higher employment (the Greek letter ρ stands for ratio). An expenditure ratio ρE greater than 1 indicates credit expansion, a ratio ρE less than 1 indicates credit contraction.

(ii) Increasing investment expenditures I exert a positive influence on employment, a slowdown of growth does the opposite.

(iii) An increase in the factor cost ratio ρF≡W/PR leads to higher employment.

The complete Employment Law gets a bit longer and contains in addition profit distribution, public deficit spending, and foreign trade.