Blog-Reference and Blog-Reference on May 3

You can make a model with the earth in the center and the planets circling around, or you can make a model with the sun in the center and the planets circling around. The model is just a realization of the underlying theory. The underlying theory in this example is the theory of gravitation which is formally encapsulated in the inverse square law. This law has NOT been found by simple observation, it has been a mental construct. Gravitation can not be seen with the two natural eyes, only with the third eye of theory.

Model building is NOT the crucial part. It is the underlying theory that is decisive. Because a well-designed theory consists of premises as foundations and the theoretical superstructure as a logical consequence the crucial part is ultimately the premises.

Standard economics is built upon this set of foundational propositions, a.k.a. axioms: “HC1 economic agents have preferences over outcomes; HC2 agents individually optimize subject to constraints; HC3 agent choice is manifest in interrelated markets; HC4 agents have full relevant knowledge; HC5 observable outcomes are coordinated, and must be discussed with reference to equilibrium states.” (Weintraub, 1985, p. 147)

Methodologically, these premises are forever unacceptable but economists swallowed them hook, line and sinker from Jevons/Walras/Menger onward to DSGE. The failure of methodological individualism is indisputable. The ultimate reason can be stated as an impossibility theorem: NO way leads from the explanation of individual behavior to the explanation of how the economic system works. The Fallacy of Composition is the lethal blunder of microfoundations.

Because of this, the microfoundations approach has already been dead in the cradle. This leaves only one option. As Joan Robinson put it: “Scrap the lot and start again.”

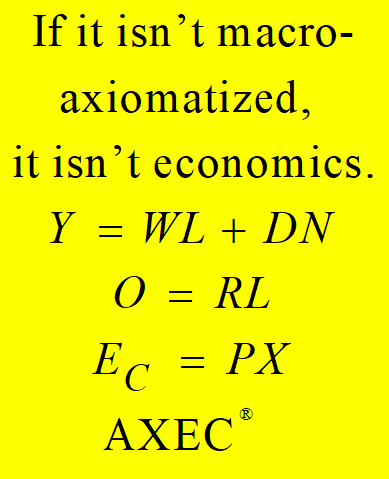

Keynes started the macrofoundations research program in the General Theory formally as follows: “Income = value of output = consumption + investment. Saving = income − consumption. Therefore saving = investment.” (1973, p. 63)

These formal foundations are conceptually and logically defective because Keynes never came to grips with profit and therefore “discarded the draft chapter dealing with it.” (Tómasson et al., 2010, p. 12).

Keynes’ original blunder kicked off a chain reaction of errors/mistakes:

• All I=S/IS-LM models are false since Keynes and Hicks (2011).

• Keynes’s profit conundrum has not been solved by After-Keynesians.

• Keynes got the Employment Law/Phillips curve wrong (2012).

So, for Keynesianism holds also: “Scrap the lot and start again.”

The situation is this: ALL models that have been built and are still being built on either the Walrasian or the Keynesian axioms are false.

What is Krugman doing? He tells on his blog: “most of what I and many others do is sorta-kinda neoclassical because it takes the maximization-and-equilibrium world as a starting point”.

From this, we can be sure that anything that Krugman ever said or will say has NO sound scientific foundation. ALL his models are defective because the Iron Methodological Law says: garbage in, garbage out. The quality of a model is determined by the scientific competence of its creator. No scientist will ever accept ‘maximization-and-equilibrium’ as a starting point for building an economic model. No scientist will ever accept Krugman.

Egmont Kakarot-Handtke

References

Kakarot-Handtke, E. (2011). Why Post Keynesianism is Not Yet a Science. SSRN Working Paper Series, 1966438: 1–20. URL

Kakarot-Handtke, E. (2012). Keynes’s Employment Function and the Gratuitous Phillips Curve Disaster. SSRN Working Paper Series, 2130421: 1–19. URL

Keynes, J. M. (1973). The General Theory of Employment Interest and Money. London, Basingstoke: Macmillan.

Tómasson, G., and Bezemer, D. J. (2010). What is the Source of Profit and Interest? A Classical Conundrum Reconsidered. MPRA Paper, 20557: 1–34. URL

Weintraub, E. R. (1985). Joan Robinson’s Critique of Equilibrium: An Appraisal. American Economic Review, Papers and Proceedings, 75(2): 146–149. URL

***

Wikimedia AXEC121i